By Michele Ford, Senior Research Analyst

Since OpenAI’s ChatGPT was introduced in late 2022, it has rapidly become a worldwide phenomenon. Supported in over 161 countries, the revolutionary chatbot gained about 100 million users within two months. But chatbots are nothing new to digitally savvy consumers.

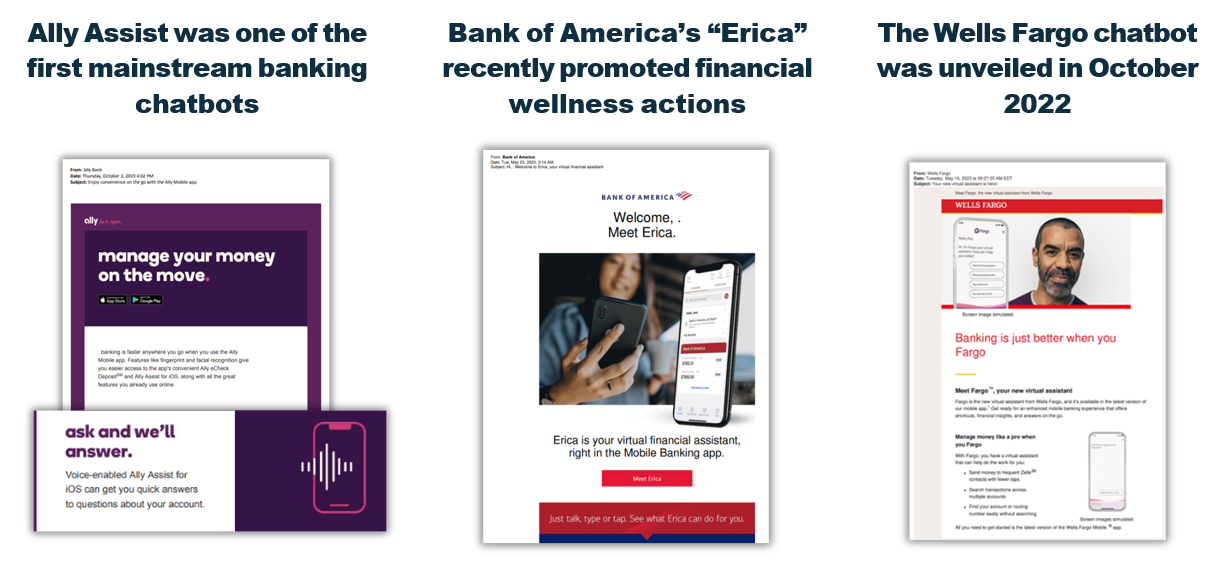

For nearly a decade, most of us have become accustomed to interacting with chatbots to manage our financial accounts. One of the first mainstream banking chatbots, Ally Bank’s “Ally Assist,” had the early functionality to transfer money, pay bills, display detailed account information, and analyze saving/spending patterns. At the time of the initial release, Ally Assist was described as being capable of “learning” from individual interactions with users. Recently, Ally Bank released an email characterizing Ally Assist (which has always been voice-enabled) in a personal way: “Ask and we’ll answer.”

Other banking chatbots were released as artificial intelligence evolved, like Bank of America’s “Erica.” A recent email communication about Erica promoted financial wellness features (personalized guidance, weekly snapshots of month-to-date spending, and account activity search). In just the last two years, both U.S. Bank (“Smart Assistant”) and Wells Fargo (“Fargo”) have launched in-house chatbots.

It is perhaps a safe bet that chatbots will continue to evolve in the banking industry. And, the prospect of harnessing a powerful artificial intelligence (AI) tool like ChatGPT may appear to bring endless possibilities.

Some Financial Firms Keeping A Respectable Distance

Even with seemingly endless capabilities, ChatGPT can and does make mistakes – an inaccuracy here, an outright fallacy there. In fact, OpenAI’s CEO Sam Altman has been transparent about ChatGPT’s reliability, tweeting “It’s a mistake to be relying on [ChatGPT] for anything important right now.” Another downside is a potential threat to privacy: conversations with ChatGPT are saved to a server for 30 days, at minimum. In addition, your inquiry about “top ways banks can use ChatGPT,” or whatever burning questions you ask can be used to train the tool (however, it is possible to opt out). But some mistakes could border on catastrophic. After Samsung employees accidentally exposed trade secrets on the platform, the company banned ChatGPT. Similarly, firms like Bank of America, Citigroup, and JPMorgan Chase have either banned or severely limited any use of the program, primarily due to compliance issues regarding third-party software.

However, Competiscan observed other financial organizations, largely investment and retirement firms, commenting on ChatGPT’s capabilities through in-house newsletters, commentaries, or social media posts. For instance, investment company Robinhood recently included a random newsbyte about ChatGPT in the firm’s monthly “Snacks” newsletter. Lending platform Upstart encouraged clients to use tools like ChatGPT to learn more about saving and budgeting. OnDeck Capital promoted the AI language model on social media as an asset to small business owners. Notably, BMO extolled the many virtues of ChatGPT, yet the company also questioned the technology’s aptitude for providing investing advice. The firm invited the social media audience to read what a “real live human” had to say on the topic.

Although banks are playing it safe with ChatGPT, a certain Buy Now, Pay Later (BNPL) firm is jumping right into the game.

Klarna Partnering With ChatGPT

Late last year, BNPL firm Klarna released a suite of technological innovations, packaged as Klarna Spotlight, in a move that distinguished Klarna from other BNPL companies. The new product featured an intelligent search tool that locates the best product prices, showcases shoppable video content and houses a Creator Platform connecting creators with retailers. According to Yahoo Finance, the Klarna app has 23 million monthly active users – with the new Spotlight platform, the brand may be poised to redefine the user experience as more shopping-focused than payments focused, creating a more loyal customer base as well as attracting new patrons.

In March 2023, Klarna announced a collaboration with OpenAI and ChatGPT to provide a “highly personalized” and “intuitive” shopping experience. The first step is installing a plug-in from ChatGPT’s website (Note: there is currently a waiting list). After the plug-in is installed, customers will receive personalized product recommendations by asking the platform for suggestions. In response, they’ll receive a curated selection of items and have the option of requesting additional recommendations. ChatGPT subscribers in the U.S. and Canada will be given priority access to the plug-in, followed by customers in other countries as the technology is continuously tested, developed and improved.

While it is impossible to know what kinds of future transformation ChatGPT will inspire, the technology could revolutionize banking through loan processing, financial planning, fraud detection, or customer service inquiries. Competiscan will continue monitoring the development and progression of ChatGPT, as well as how financial institutions respond and adapt to it.