By: Jessica Duncan, AVP Research & Insights

It’s been six months since Silicon Valley Bank (SVB) collapsed at a shocking speed, taking just 48hours to go from solvent to shut down by regulators. This event sparked panic in the following days, and to prevent further contagion regulators took action with several other banks, including the shutdown of Signature Bank.

In March 2023, Competiscan shared the immediate response trends taken by financial institutions to alleviate customers’ concerns. As reported, the marketing tactics largely fit into three themes:

- Reassure customers their deposits were safe

- Educate customers on why SVB was shut down

- Convey the institution’s resiliency and stability

But what happened next? After the shock died down, did this historical moment impact how financial institutions further communicated with their customers? Find out below as we feature financial institutions that are doing more than their legal obligation and including stronger marketing emphasis on deposit coverage and institutional security.

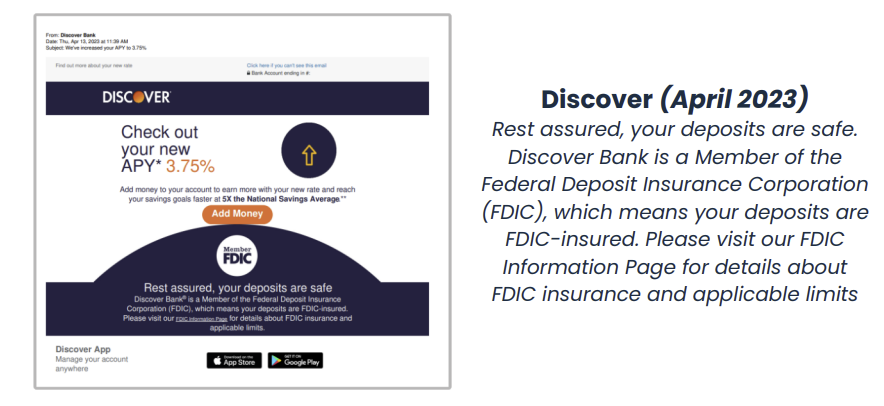

More Than Just a Footnote

What the law required was typically what financial institutions used to disclose their FDIC or NCUA insurance. But how many consumers ever notice or read the fine print? In April, Discover introduced a banner that included the Member FDIC logo and a supporting paragraph explaining that customers could “rest assured” that their deposits were safe. Discover is still incorporating this design element in its marketing today.

American Express cited “FDIC Insured” as one of three benefits featured within a blue border at the bottom of emails related to its High-Yield Savings account. This border also drew attention to key benefits, like “No Fees” and “No Minimum Balance.” Recently, EverBank used the coveted first bullet in the body of a CD acquisition email to disclose FDIC coverage details, a spot typically reserved for the leading benefit. Despite being placed below the fold, Citibank gave spotlight to the “peace of mind” of FDIC insurance within a block of text related to simplifying your savings routine.

Also, Commerce Bank built FDIC Insurance into the headline of a CD mailer by stating, “We’re built for what matters to you, like a fixed rate of return and FDIC Insurance.”

What Does the Coverage Actually Mean?

What Does the Coverage Actually Mean?

Prior to this incident, how many individuals thought about what the coverage meant or how it applied to their accounts and deposit balances? Some institutions took to social media to offer better explanations and to help consumers understand FDIC or NCUA deposit coverage.

Just this week, Ally Bank released a sponsored social advertisement with the title “Do you know what the FDIC is?” The post featured a video of individuals being stopped in the street and asked this question. The ‘Learn more’ link in the ad redirected readers to a landing page on Ally’s site that offered information on the topic, including a well-designed infographic on how to maximize FDIC coverage.

In closing, it’s an optimistic sign to see financial institutions be more transparent and work to education consumers about how deposits are protected. There is no downside for a financial institution to take these steps. The efforts will likely be perceived positively and can build brand identity, consumer trust, or even differentiate the institution. Whatever the reasons may be, let’s hope these efforts stick around as consumers deserve to be in the know.

In closing, it’s an optimistic sign to see financial institutions be more transparent and work to education consumers about how deposits are protected. There is no downside for a financial institution to take these steps. The efforts will likely be perceived positively and can build brand identity, consumer trust, or even differentiate the institution. Whatever the reasons may be, let’s hope these efforts stick around as consumers deserve to be in the know.